RBI’s Annual Basic Statistical Return (BSR)-1 on Credit by Scheduled Commercial Banks – March 2026.

Mumbai; May 2026: Today (Friday – 29th May 2026) the Reserve Bank Of India has released the web publication ‘Annual Basic Statistical Return (BSR)-1 on Credit by Scheduled Commercial Banks – March 2026 on its ‘Database on Indian Economy’ (DBIE) portal.

The publication provides information on various characteristics of outstanding bank credit in India, based on data submitted by SCBs {including Regional Rural Banks (RRBs)} under the annual Basic Statistical Return (BSR)–1 system, which collects information on type of account, organisation, occupation/activity and category of the borrower, district and population group of the place of utilisation of credit, rate of interest, credit limit and amount outstanding. Further, a new data series presenting district level gender wise information on outstanding credit to individuals is included in the publication from this round.

Highlights:

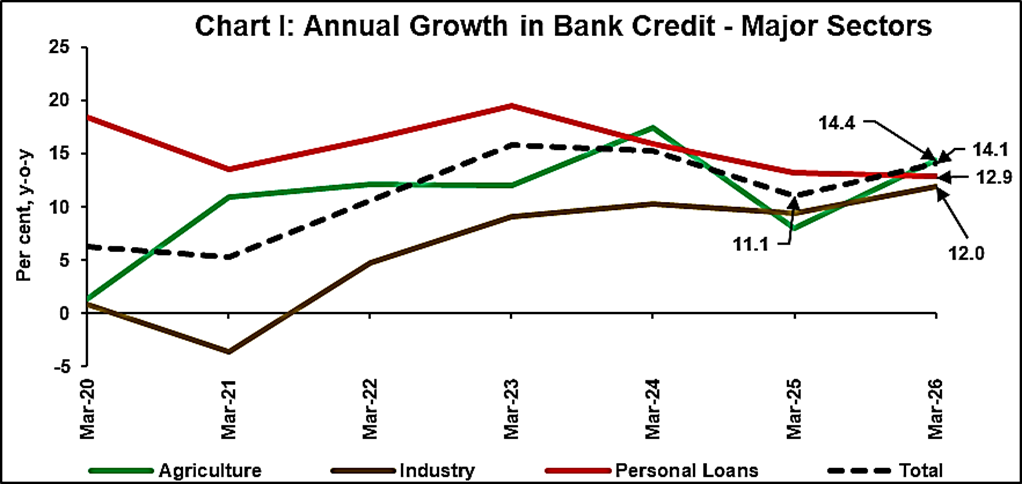

- Bank credit growth (year-on-year) have increased to 14.10% as on 31st March 2026 from 11.10% a year ago (Chart I).

- In line with the monetary policy actions during FY 2025-26, the share of loans bearing interest rates of less than 9% increased to 64.2% as on end-March 2026 from 43.9% a year ago.

- Credit growth (y-o-y) across all population groups, viz., rural, semi-urban, urban and metropolitan, exhibited sustained expansion, maintaining double-digit growth as on end-March 2026. The respective shares of lending by rural, semi-urban, urban and metropolitan bank branches stood at 9.4%, 14.5%, 17.9% and 58.2%.

- Private sector banks witnessed increase in credit growth (y-o-y) to 12.3% as on end-March 2026 from 9.5% a year earlier. While their counterpart public sector banks recorded higher credit growth than headline credit growth. Small finance banks continued to sustain higher credit growth, expanding their total credit share to 1.6% from 1.0% in March 2021.

- Personal loans growth (y-o-y) moderated to 12.9% as on end-March 2026, falling below overall credit growth after consistently outpacing it over the past several years (Chart I). The share of personal loans within total credit remained significant and stood at 30.7%.

- Loans to private corporate sector accounted for more than one fourth of total bank credit and grew (y-o-y) by 15.5% as on end-March 2026 from 11.9% a year ago.

- Credit growth (y-o-y) in the agriculture and industrial sectors increased to 14.4% and 12.0%, respectively, as on end-March 2026 from 8.1% and 9.4% a year ago. Their shares in total bank credit stood at 12.9% and 22.4%, respectively, as on end-March 2026.

- Borrowings by the household sector increased by 14.3% (y-o-y) as on end-March 2026. The sector’s share in total bank credit stood at 58.6% and accounted for about three fifths of the incremental credit during FY 2025-26.

- The share of individuals in total bank credit remained at 47.8% as on end-March 2026. Within this segment, the share of female borrowers stood at 24.7%, marginally up from 23.8% a year ago.

- The share of term loans in total bank credit stood at 62.8% as on end-March 2026. Within term loans, the share of loans bearing interest rates of less than 10% stood at 80.2%.

Team Maverick.

Shivakumar Says Congress United, Assures Women Will Get Cabinet Berth

Bengaluru, Aug 2026 : Karnataka Chief Minister D.K. Shivakumar on Monday sought to dismiss…

Shivakumar Says Congress United, Assures Women Will Get Cabinet Berth

Bengaluru, Aug 2026 : Karnataka Chief Minister D.K. Shivakumar on Monday sought to dismiss …