Steel Companies In Non-OECD Countries, Particularly China, Receive Higher Subsidy Levels than OECD Countries.

December 2025: The Organisation for Economic Cooperation and Development (OECD) draws on a confidential database to track different types of industrial subsidies. The Manufacturing Groups and Industrial Corporation (MAGIC) database comprises extensive and comparable financial data, as well as below market borrowing (BMB) estimates, for a sample of 47 steel firms covering 36% and 62% of steelmaking capacity in OECD member countries and in non-OECD countries respectively, as of 2022, and from the year 2005 to 2022.

Manouvering this data, the OECD published a new report in October, 2025, “The drivers and impacts of subsidies to steel firms”. The study finds that steel firms in non-OECD countries, especially in China, receive far greater subsidies than firms in OECD countries. The findings highlight the challenges that the provision of subsidies to steel firms, especially in non-OECD countries, can represent for the pursuit of a fairer and more competitive steel market.

Why is the policy brief important?

The non-market subsidisation practices of some countries, particularly China, have contributed to global overcapacity in steel, aluminium, semiconductors, and other industrial goods, plunging global prices to the point where firms in OECD countries struggle to compete. Given that World Trade Organization (WTO) rules were not designed to tackle such non-market practices, OECD countries are left with little recourse (though the United States has imposed tariffs under national security grounds in part to address overcapacity).

Discussions on addressing overcapacity in the steel sector are organized under the Global Forum on Steel Excess Capacity (GFSEC) which is facilitated by the OECD. This new report can help guide 2026 GFSEC discussions, providing details on the types of subsidization that are fuelling overcapacity. Better understanding these non-market conditions could provide clues to building a more level playing field for firms in OECD countries in the future.

What’s in the policy brief?

The OECD’s report includes two principal sections:

- Data-driven chapters analysing results from the MAGIC database: subsidies are pervasive but very unequally distributed; subsidies to steel firms are driven by several factors; and the impact of subsidies on crude steelmaking capacity

- Policy recommendations and proposed way forward.

How to find the key insights –

Data-driven Chapters:

- Subsidies to steel firms are widespread, persistent, and delivered through multiple instruments. Using the OECD MAGIC database (2005–2022), the report finds that nearly all observed steel firms receive government support in some form, only 06% of firm-year observations show zero subsidies, while about 90% of firms receive subsidies in at least half of their observed years. Main subsidy instruments include: cash grants and transfers (direct financial support for projects, equipment, upgrades, or cost reimbursements); below-market borrowings (BMB) (preferential or implicitly guaranteed loans from state-controlled or influenced lenders); and corporate income-tax concessions (tax exemptions, reduced rates, credits, or benefits linked to investment or performance).

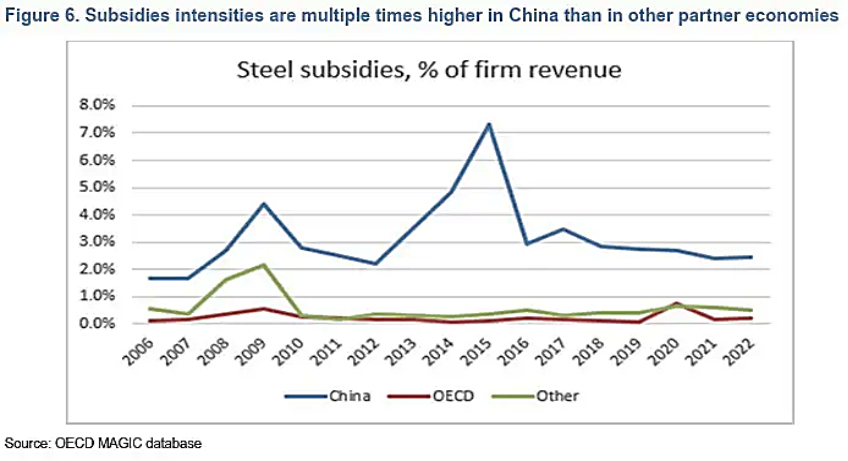

- Subsidies fluctuate substantially, increasing sharply during crises. In the 2009 global financial crisis and China’s 2015–2016 slowdown, BMB surged. Subsidy intensity (subsidy size relative to firm size) varies widely: China’s subsidy intensity is five times higher than that of other non-OECD countries and 10 times higher than OECD countries. Key firm characteristics influencing the size and likelihood of subsidization include home jurisdiction, firm size and the degree of state ownership. The percentage of state ownership is more informative than a binary state-owned enterprise (SOE) vs. non-SOE classification, and higher government ownership strongly correlates with receiving larger subsidies relative to firm size.

- Steel firms with higher state ownership receive significantly more subsidies across all instruments: Firms with >25% state ownership receive twice as much in grants and tax concessions (relative to asset size) as firms with <10% state ownership. They receive three times more BMB. This reflects both direct support (grants, tax benefits) and indirect support (cheaper or guaranteed loans).

- Higher state ownership also implies higher indebtedness and lower profitability. State-owned or state-influenced firms tend to be more indebted, with debt-to-asset ratios around 30% higher. Such firms are less profitable, with return on equity and return on assets almost three times lower for majority-owned SOEs. In China, SOE’s debt-to-capacity ratio is 2.5 times that of private firms, showing deep structural imbalances driven by state support.

- State ownership is the primary driver of subsidy allocation. Once ownership share is controlled for, profitability indicators generally do not predict subsidies. In OECD countries, higher debt results in fewer subsidies. However, in non-OECD countries the data shows that more debt can result in mores subsidies (no negative effect). Firm size also matters, with larger asset bases likely to attract more subsidies in non-OECD countries. Global steel demand is usually not significant in subsidy allocation. China is the exception; Chinese SOEs maintained very high utilization rates (84% vs. national averages ~65%), implying government support sustained production even in weak markets.

- There is a correlation between subsidies and overcapacity. Cash grants increase steel production capacity, but only in non-OECD countries, not in OECD countries. In non-OECD countries, a sustained USD 1 million annual grant is linked to a 5,000–15,000 ton capacity increase. No measurable impact is found from grants in OECD members. BMB’s effects are complicated by endogeneity: governments often provide BMB during crises, making rising BMB appear negatively correlated with capacity due to reverse causality. BMB likely helps maintain existing capacity during downturns rather than expand it. Using instrumental variables to isolate the exogenous component of BMB, a USD 1 million increase in BMB is linked to a 1,000 ton capacity increase. This is smaller than the grant effect but reflects a structural (non-crisis) contribution to capacity growth.

How to apply the insights –

- Utilising data from the MAGIC database, the data-driven chapters of “The drivers and impacts of subsidies to steel firms” highlight specific steel firm’s characteristics that are driving the provision of subsidies, and the differences of such drivers in OECD and non-OECD countries, as well as the impact of subsidies on steel firms’ crude steelmaking capacities.

- Government subsidies enable larger firms, more indebted firms, and firms with greater government ownership to expand capacity beyond market-driven levels in normal times, and to maintain capacity during subsequent steel industry crises.

- These subsidies distort market signals, allowing subsidized firms to continue operating while depressing global steel prices, which disproportionately affects unsubsidized firms by eroding their profit margins.

How to find the key insights –

Policy recommendations and proposed way forward:

- The authors recommend enhancing transparency concerning loan terms to help in accurately identifying the source of BMB. They highlight the widespread use of the principles of non-discrimination set out in the OECD Recommendation on Competitive Neutrality, which could be more broadly applied in non-OECD countries. Given that grants and BMB are strongly correlated with higher government ownership, the authors suggest improving the fairness and transparency of these subsidy processes.

- Given that BMB plays a role in preventing the withdrawal of production capacity during downturns, thereby delaying market-driven restructuring, efforts should be undertaken to ensure such efforts do not impede necessary capacity reductions. Governments need to be mindful of the tendency to favour larger firms and those with greater government ownership, and seek to mitigate risks of creating market distortions and moral hazard (e.g., a “too big to fail” situation). Governments should be more wary of subsidizing steel firms in poor financial conditions, as such subsidies are more likely to be used to maintain or expand capacity.

- Further analytical studies are recommended to examine the impact of steel subsidies on recipient steel firms’ market shares, as even subsidies that do not directly increase net crude steelmaking capacity or affect their usual financial ratios may still have a distortive effect.

How to apply the insights –

- Taking into account the findings from the MAGIC database, policy makers should utilize opportunities in various global forums to advocate for greater transparency into subsidies in the steel sector, particularly through the 2026 GFSEC meetings.

- Engagement should also focus on promoting market-driven restructuring and reducing subsidies to failing firms that contribute to overcapacity.

- Policymakers need to coordinate their policy efforts to tackle distortive subsidies and their effects. Continued analysis is necessary, as the impact of steel subsidies on firms’ market shares could provide further insights.

Conclusion –

Firms in several countries are negatively affected either directly or indirectly by certain types of subsidisation that contribute to overcapacity in the steel sector. Gaining a better understanding of the root causes of overcapacity and how specific types of subsidization can drive overcapacity could help global policymakers develop equitable solutions. Government participation in dedicated global initiatives such as the GFSEC and promoting greater transparency and adherence to competitive neutrality can potentially result in meaningful outcomes in 2026.

Team Maverick.

Shivakumar Says Congress United, Assures Women Will Get Cabinet Berth

Bengaluru, Aug 2026 : Karnataka Chief Minister D.K. Shivakumar on Monday sought to dismiss…

Shivakumar Says Congress United, Assures Women Will Get Cabinet Berth

Bengaluru, Aug 2026 : Karnataka Chief Minister D.K. Shivakumar on Monday sought to dismiss …