Assam: Comptroller And Auditor General Of India Tables Report For The Period Ended March 2024; Large Scale Financial Irregularities Unearthed.

Guwahati/New Delhi; May 2026: Maverick News 30 in its report dated 25th May 2026, had reiterated that, The Comptroller and Auditor General’s (CAG) Audit Report on State Finances for 2024-25, was tabled before the state legislature this month. The 235 pages report analysed by Maverick News 30 unveils major financial irregularities in each and every sphere.

Performance Audit (PA) on the Functioning of District Transport Offices –

The Transport Department is the fourth-largest revenue generating Department for the state, accruing income through vehicle taxation, licensing fees, permit charges, and penalties. The audit identified systemic inefficiencies, regulatory non-compliance, and revenue leakage across critical operational domains.

- Against a significant proportion (7.85%) of issued Learner’s Licenses and Driving Licenses, no dates of driving test were recorded, raising concerns regarding licensing practices without due evaluation. Analysis of driving test slots revealed improbably high daily testing numbers in 24 of 40 cases during 2019-24, indicating potential procedural lapses or compromised assessment rigor.

- In the course of test check of records of VAHAN database for the seven States of North Eastern (NE) Region with that of Assam, it was observed that a total of 15,849 vehicles having same chassis number and engine number were registered in multiple states. Out of these 15,849 vehicles, 12,112 vehicles (76%) were allowed subsequent registration in Assam without NOC, which was irregular.

- Significant deficiencies were observed in issuance of transport vehicle permit across eight test checked DTOs, with only 26,105 permits (21.87 per cent) issued against 1,19,369 registered vehicles (2019-24). The lack of stringent permit enforcement led to revenue losses, regulatory gaps, and proliferation of unregulated commercial transport operations.

- School buses across eight districts (2019-24) were issued contract carriage permits instead of Educational Institution Bus (EIB) permits resulted in the bypassing of mandatory fitness tests, thereby defeating the purpose of EIB permits, which are specifically designed to ensure enhanced safety standards for school transportation. The absence of recorded reasons for this deviation raises concerns about regulatory lapses and possible procedural irregularities by the DTOs.

Non Production Of Records –

Non-production of records constituted 50% of the sample size and potential risk of Rs. 7.162 Crores could not be addressed. In these cases, the basic records such as financial statements, GSTR-9C wherever applicable and GSTR-2A were not produced and hence could not be audited. Similarly, the specific taxpayer records (granular records) sought for based on identified risks were partially produced in 14% of cases; as a result, the identified risks relating to excess/irregular ITC availment and undischarged liability of Rs. 0.751 crore could not be examined in detail by Audit. In the Exit Conference, it was stated (March 2025) that an advisory related to the production of records would be issued to all unit offices.

Performance Audit (PA) Of The Process Of Manufacturing, Distribution And Sale Of Alcoholic Products –

The PA brought out various deficiencies in regulations as well as effective compliance of rules, which are discussed in the succeeding paragraphs.

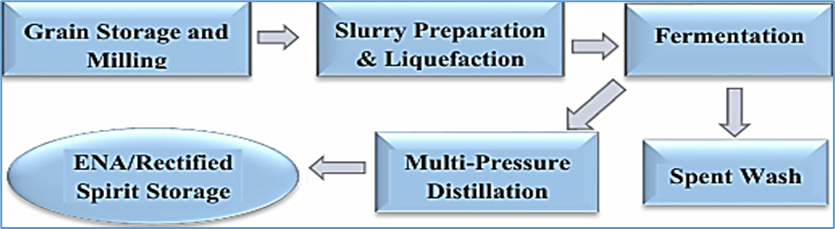

There are two distilleries in Assam, namely M/s Brahmaputra Biochem Private Limited, Kamrup, and M/s Radiant Manufacturers Private Limited (Distillery Division), Karbi Anglong which are manufacturing Extra Neutral Alcohol (ENA) and Rectified Spirit (RS) from grains (rice, maize, etc.). The following block diagram displays the manufacturing process of alcohol:

Norms prescribed for manufacture of any product in proportion to the raw material consumed by the industry, is a prime control mechanism to exercise control on the quantum of alcohol actually produced in the State as well as to safeguard the interests of the State against the possibility of under disclosure of production by the manufacturers.

It was observed that the Government of Assam did not prescribe the norms or standard (i.e., input-output ratio) regarding production of alcohol (ENA or RS) from grains. It is pertinent to mention here that Rajasthan, Andhra Pradesh, and the neighbouring State Meghalaya has prescribed norms for production of alcohol from grains.

The absence of prescribed input–output norms for production of Extra Neutral Alcohol (ENA) or Rectified Spirit (RS) from grains represents a critical regulatory gap. Such norms are a fundamental control mechanism used by other States, including Rajasthan, Andhra Pradesh, and neighbouring Meghalaya, to verify production yields, prevent under-reporting, and ensure accurate tax assessment. Without these standards, manufacturers can understate production volumes, leading to potential large-scale revenue leakage for the State. The Department’s acceptance of this weakness and commitment to study other States’ models underscores the urgent need to establish clear, enforceable norms to strengthen excise administration and safeguard public revenue.

In the exit conference (February 2025) as well as in its subsequent reply (February/April 2025), the Department stated that decision would be taken to issue notifications in this matter after studying the rules/ norms framed by other States.

Performance Audit (PA) Of The Process Of Manufacturing Of Beer From Malt, Rice Flakes, Sugar, Hops, At Breweries –

The Government did not prescribe the norms or standard (i.e., input-output ratio) regarding production of beer from broken rice, malt, sugar, hops, etc. Other State like Rajasthan prescribed the norms for maintaining minimum yield of Beer from Malt or other raw materials.

Para 677 (17) of the Manual of Excise & Salt Department, 1918 prescribes the norms for raw material as 15.42 kg of Malt or 14.52 kg of rice flakes or 12.70 kg of sugar for production of 81.823 BL of wort. Breweries are using ‘batch fermentation’, whose minimum efficiency is 90% for grains as per the information provided by NSI, Kanpur.

Audit observed from relevant records that these breweries had consumed 246.71 lakh kg of malt, 128.36 lakh kg of rice flakes and 36.30 lakh kg of sugar and produced 1809.00 lakh BL of beer during the period from 2018-19 to 2023-24. However, as per the norms prescribed in the Manual of Excise & Salt Department, 1918, the minimum yield of beer (using the above-mentioned quantities of ingredients) should have been 2,039.71 lakh BL, thereby depicting a shortfall of 230.71 lakh BL – indicating potential under-reporting and risk of excise duty loss. This highlights a critical regulatory gap that requires urgent attention through introduction of a clear, enforceable production standards.

In the exit conference (February 2025) followed by the formal reply (February/April 2025), the Department stated that necessary decision in this regard would be taken after studying the relevant rules framed by other states and also stated that such issue would be addressed through suitable notifications to be issued shortly.

Performance Audit (PA) Of The Process Of Manufacturing Of Drought Beer –

As per Rule 498 (c), “Draught Beer” means fresh beer contained in a keg not more than 05% volume by volume (v/v) alcoholic content. Further, as per Rule 19 (a) (I), the Ad-valorem levy on draught beer shall be charged on basis of its daily installed capacity @ ₹50 per BL, which was reduced to @ ₹32 per BL31 (w. e. f. 12/02/2021).

In respect of 25 types/ flavour of beer (out of 40 types/ flavour) produced by the five Microbreweries, in one of the batches produced, the alcoholic content was more than 05% (v/v) as per the Chemical Examiner Report and as per the information furnished by the concerned Microbrewery.

Audit concludes that production and sale of draught beer exceeding the 05% v/v legal limit by microbreweries in Assam represents clear violation of Rule 498 (c) of Assam Excise Rules, 2016. Despite chemical evidence confirming this non-compliance, the Department did not enforce rules effectively, citing absence of enabling provisions, which undermined regulatory credibility and allowed unapproved higher-strength beer to be sold.

In the exit conference (February 2025), the Commissioner & Secretary, Excise Department instructed the Departmental officers to take necessary action against those microbreweries, which served draught beer with alcohol content beyond 05%, as per law.

Performance Audit (PA) Of The Process Of Regulating The Adhesive Hologram –

Rule 582 of the Assam Excise Rules, 2016 stipulates the system of procurement of Holograms from the manufacturer. The licensee of a Foreign Liquor manufactory, Brewery, Country Spirit manufactory,

Heritage Alcoholic Beverages manufactory and Wholesale warehouses, in case of Import, shall make advance payment (in form of Demand Draft in favour of the hologram manufacturer) for the procurement of hologram to the Commissioner of Excise, Assam.

On approval of the requisition/indent, a pass will be issued authorising the supply of holograms to the concerned manufactory. The manufacturer shall arrange to dispatch the holograms within 72 hours of receiving such intimation from the Excise Commissioner.

During February 2022 to March 2023, a total of 564 indents were received from licensees through the Commissioner of Excise, Assam for supply of 74,82,30,000 numbers of Holograms and the same were also supplied to the concerned manufacturers/ wholesale warehouses.

Audit noticed that out of 564 indents, 45,60,00,000 numbers of Holograms against 219 indents (39%) were supplied after delays ranging from 1 to 24 days (average: 03 days) beyond the stipulated period of 72 hours, which contravened the rules.

On receipt of the Holograms, the Excise Officer-in-charge of Foreign Liquor manufactory, Brewery and

Country Spirit manufactory shall confirm the receipt through a verification certificate. This mechanism aimed to have assurance that the dispatched quantities of holograms have reached the bona-fide users and not any unscrupulous third party.

During February 2022 to March 2023, a total of 74,82,30,000 Holograms against 564 indents were supplied to the concerned manufacturers/wholesale warehouses. However, neither did the Officer-in-charge of Foreign Liquor manufactory, Brewery and Country Spirit manufactory have submitted the confirmation of receipt of holograms (through a verification certificate) nor did the Commissioner of Excise, Assam ask for confirmation certificates.

Audit concludes that the Excise Department did not enforce Rule 582 of the Assam Excise Rules, 2016, by not obtaining mandatory verification certificates confirming receipt of 74.82 crore holograms supplied between February 2022 and March 2023.

This critical control lapse created a significant risk of diversion of holograms, if any, to unauthorised or illicit liquor manufacturers, remaining undetected, undermining excise duty safeguards and enabling potential counterfeit production. The Department’s claim of confirmation in the AERMS portal is not supported by the provided data, which showed blank confirmation fields. This reflects serious weaknesses in monitoring, documentation, and enforcement of excise controls essential for revenue protection and public safety.

Taken together, the findings paint a picture of systemic financial indiscipline – one that the CAG has now placed squarely before the Public Accounts Committee for “discussion and suitable recommendations”.

[Team Maverick is going to publish the report in the forthcoming episodes].

Suvro Sanyal; Team Maverick.

Governor pays obeisance at Baba Lal Ji Dhianpur Dham

On the eve of Guru Purnima, Governor Kavinder Gupta along with Lady Governor Bindu Gupta t…

Governor pays obeisance at Baba Lal Ji Dhianpur Dham

On the eve of Guru Purnima, Governor Kavinder Gupta along with Lady Governor Bindu …