World Bank issues the Global Findex 2025.

The Global Findex Database is the world’s only demand-side survey on financial inclusion and a leading source of data on how adults around the world access and use financial services. Since its launch in 2011, the Global Findex has provided critical insights into financial inclusion, digital payments, savings, and borrowing behaviors across various economies. The database highlights key trends such as the rise of digital financial services and the gender gap in account ownership.

The Global Findex 2025 introduces the Digital Connectivity Tracker, a new component that measures access to and use of mobile technology. Combined with financial inclusion data, it offers a holistic view of how mobile infrastructure is expanding access to financial services and improving economic resilience.

The key take aways of the Findex 2025 are:

- Worldwide, 79% of adults have an account at a bank or similar financial institution, with a mobile money provider, or both, up from 74% in 2021.

- Worldwide, 86% of adults own a mobile phone, though smart phones are less common in some regions.

- Gender gaps in account ownership have narrowed, and gender gaps in mobile phone ownership are small – Globally, 81% of men and 77% of women have accounts — representing a gender gap of 4 %age points. Low & middle-income economies show a similar gender gap, at 5 %age points, with 78% of men and 73% of women having an account.

- Global Findex 2025 finds that of the 1.3 billion adults globally without accounts:

- More than 700 million (55%) are women.

- 670 million (52%) are from the poorest 40 % of households by income.

- 790 million (62%) have a primary education or less.

- 690 million (54%) are either out of the workforce or unemployed.

- 380 million (29%) are aged 15 years to 24 years, another 590 million (46%) are aged 25 years to 54 years, and 320 million (25%) are aged 55 years and older.

- Formal saving has surged globally, enabled by mobile accounts and breaking a long-term trend of slow growth.

- More adults are making digital merchant payments

- Across low- and middle-income economies, 61% of adults, or 82% of account owners, made or received a digital payment in 2024, a 27 %age point increase from 2014.

- Despite advances, many remain without mobile phones or financial accounts and require focused programs – women are disproportionately less likely than men to have accounts, and being poor remains the biggest barrier to financial access, as adults living in poorer households make up a disproportionate share of people without accounts.

- Increased digitalisation and mobile financial adoption come with risks, and not everyone is adequately protected – In Sub-Saharan Africa, only about half of the region’s 300 million mobile money account owners protect their phones with passwords. Around the world, women are less likely than men to have passwords.

- Opportunities remain to better equip people to leverage financial services to reach their goals and increase resilience – just 56% of adults could easily access extra money to deal with an unexpected event such as a loss of income or an accident.

- Many of the world’s 1.3 billion people without financial accounts already have the tools they would need to get financial services.

- Costs come up again as a barrier in the context that many people use someone else’s phone rather than owning their own. In South Asia, 49% of adults who do not own a mobile phone use someone else’s, and in Sub-Saharan Africa 31 % do. Non-owning phone users present an opportunity to increase connectivity, since this group already shows demand for and some skill with digital devices.

- Informational activities such as consuming news and learning are also popular – In low- and middle-income economies, 39 % of adults and 71% of internet users read or watch the news online; A relatively small share of adults uses online channels to earn money or search for a job – only 6% of adults in low- and middle-income economies and 11% of internet users use apps or websites to earn money. Outside East Asia and Pacific, where 12% of all adults earn money on the internet—more than 10% of adults in every economy in the region—only a small number of economies breach the 10% threshold: Argentina, Eswatini, and Iraq, with 11%; Brazil, Mauritania, and South Africa, with 12%; Lesotho, with 13%; Senegal, with 15%; Belize, with 16%; and Namibia, with 17%. All have mobile phone ownership rates near or above 80%.

- Data costs are a barrier to more, and more frequent, internet use in low & middle-income economies – Monthly unlimited data plans for mobile phone owners are uncommon outside high-income economies. Instead, people buy a certain amount of data (1 gigabyte, for example), and then top up their data when they run low. This can be prohibitively expensive,

- In low- and middle-income economies, only 60% of mobile phone owners have a password on their mobile phones; more men than women mobile phone owners have passwords on their devices – in most economies, between 15% and 30% of phone owners with passwords cannot change them. This could be for benign reasons. For example, a shopkeeper or a more digitally skilled family member may have helped set up a user’s phone and its password at purchase, after which the owner forgot the steps for changing it. Phones passed down after a family member upgrades to a more recent model may also have the original owner’s password.

- Exposure to scams or extortion attempts is high among online users, though few lose money to them. Exposure to digital exploitation is more common than online harassment. In low and middle-income economies, 14% of adults, or 19% of phone owners, report having received a text or SMS message from someone they don’t know asking for money in the context of a scam or online extortion.

- Ownership of ID is nearly universal across regions except for Sub-Saharan Africa – ID matters for connectivity and accessing financial services, among other benefits. People without ID face challenges participating in important activities. Specifically, people without ID often have difficulty buying SIM cards; participating in elections; accessing financial services, government support, and medical care; and applying for jobs.

- Financial Access – Globally, unless otherwise noted:

- 79% of adults have an account, which is an increase of 28% age points since 2011.

- 75% of adults in low- and middle-income economies have accounts.

- 77% of women have an account, narrowing the global gender gap to 4% age points.

- Over half of all adults in low and middle-income economies now make payments from an account using a mobile phone or card.

- Mobile Money accounts have spread worldwide. 15% of all adults now have one.

(vi) In Sub-Saharan Africa and Latin America and the Caribbean – Around 40% of adults have mobile money. angles-down Poorer adults are still 11% age points less likely than wealthier adults to have an account.

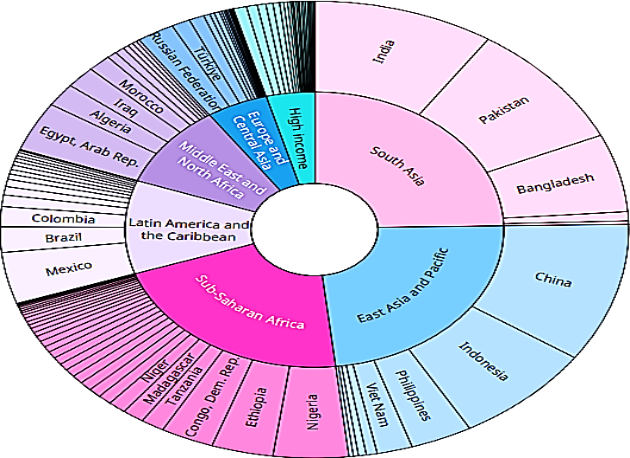

- 1.3 billion adults worldwide still lack accounts. 650 million of them live in just eight economies.

- Adults without accounts who own a mobile phone, basic ID, and a SIM card registered in their name have the foundations for account ownership. there are 80 million of them in Sub-Saharan Africa alone.

- Affordability, accessibility, and not having enough money to use accounts are the top three barriers to having one in low and middle-income economies.

- The share of adults borrowing formally by using credit cards was generally small, though this type of borrowing dominated in a few low and middle-income economies. In low and middle-income economies in 2024, just 15% of adults used a credit card in the past 12 months.

- India has made progress in increasing the share of adults with active accounts. Despite its comparatively low rate of active accounts, both the absolute number and the % age of adults with active accounts in India has increased. In addition, more men than women own active accounts, though the gender gap in ownership of active accounts as a % age of account owners fell from 12% age points in 2021 to 7% age points in 2024. This decrease may be due to the large increase over the same period in women receiving government to-person (G2P) payments digitally, from 13% in 2021 (59% of women receiving a G2P payment) to 24% in 2024 (81% of women receiving a G2P payment).

- Financial Health – In low- and middle-income economies, People are financially healthy when they can manage their needs, pursue opportunities, deal with financial emergencies, and feel confident about their finances. About a third of adults could cover more than two months of expenses if they lost their main income source.

- Financial Worry – People worry about having enough money for monthly expenses, medical bills, school fees, old age, and business expenses. The monthly expenses are the most common source of financial stress, followed by medical expenses. In South Asia and Sub-Saharan Africa about 20% of adults worry about school fees. 26% of adults worry about having enough money for old age, yet only 18% of adults save formally and for their retirement.

- About 10% of adults received international remittances in Latin America and the Caribbean.

- 56% of people could reliably get hold of extra money to deal with an emergency. Family or friends are the most popular source of extra money, though savings are more reliable. Women and poorer adults are more likely to rely on family or friends for additional funds.

- One in four adults experienced a natural disaster in the past three years. Two-thirds of them lost their income or an asset.

- Around 1 in 4 Mobile Money Account owners in Sub-Saharan Africa sent a payment to the wrong person. Half never got their money back.

- Around 40% of bank account owners have checked their account balances with their phone or a computer, and the same share have received account information via email or text.

Team Maverick……….

Deschamps Admits France Fell Short as Spain End World Cup Dream with 2-0 Semifinal Win

Arlington (Texas), July 2026 : France head coach Didier Deschamps admitted his side was ou…

Deschamps Admits France Fell Short as Spain End World Cup Dream with 2-0 Semifinal Win

Arlington (Texas), July 2026 : France head coach Didier Deschamps admitted his side was …