Bank Of Japan’s Monetary Policy Highlights The Economy Is Likely To Continue Growing Moderately.

Tokyo; February 2026: Japan’s economy is likely to continue growing moderately, with overseas economies returning to a growth path, and with support from factors such as the government’s economic measures and accommodative financial conditions, while the economy is projected to be affected by trade and other policies in each jurisdiction.

Inflation is likely to move toward around 02%: The year-on-year rate of increase in the CPI is likely to decelerate to a level below 02% in the first half of this year. However, underlying CPI inflation, which excludes temporary fluctuations, is likely to continue rising moderately. Thereafter, as the economy continues to improve, it is expected that the rate of increase in the CPI and underlying CPI inflation will increase gradually and then be at a level that is generally consistent with the price stability target of 02%.

Developments in overseas economic activity and prices, wage, and price-setting behavior of firms, market developments, etc. warrant attention: Risks to the outlook for Japan’s economic activity and prices include developments in overseas economic activity and prices under the impact of trade and other policies in each jurisdiction, wage- and price-setting behavior of firms, and developments in financial and foreign exchange markets, and these risks require attention.

Bank will conduct monetary policy with the 02% target: As for the conduct of monetary policy, if its outlook for economic activity and prices will be realized, the Bank, in accordance with improvement in economic activity and prices, will continue to raise the policy interest rate and adjust the degree of monetary accommodation.

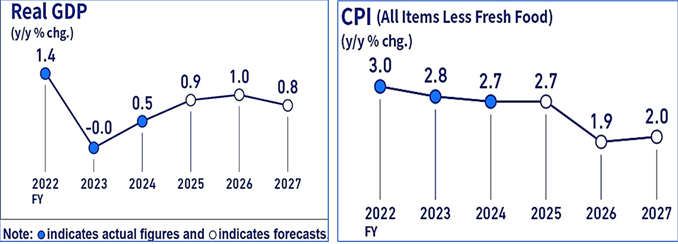

Policy Board Member’s Forecasts: The member’s forecasts have been provided below:

Japan’s economy has recovered moderately, although some weakness has been seen in part. Overseas economies have grown moderately on the whole, although some weakness has been seen in part, reflecting trade and other policies in each jurisdiction.

Exports and industrial production have continued to be more or less flat as a trend, while they have been affected by the increase in U.S. tariffs. Corporate profits have remained at high levels on the whole, although downward effects due to tariffs have been seen in manufacturing, and business sentiment has been at a favorable level. In this situation, business fixed investment has been on a moderate increasing trend. Private consumption has been resilient against the background of an improvement in the employment and income situation, although it has been affected by price rises. On the other hand, housing investment has declined.

Meanwhile, public investment has continued to be more or less flat. Financial conditions have been accommodative. On the price front, with moves to pass on wage increases to selling prices continuing, the year-on-year rate of increase in the CPI (all items less fresh food) has been at around 2.5% recently, due to the effects of the rise in food prices, such as rice prices, and other factors. Inflation expectations have risen moderately.

Baseline Scenario of the Outlook for Economic Activity –

Corporate sector: although downward pressure stemming from the impact of tariff increases is expected to remain for the time being, exports and production are likely to recover moderately as overseas economies return to a growth path, partly supported by global AI-related demand. Corporate profits for the time being are likely to remain at high levels on the whole, although downward effects due to tariffs are expected to continue to be seen in manufacturing; thereafter, the uptrend in corporate profits is likely to become more pronounced due to an increase in domestic and external demand. In this situation, supported in part by the government’s economic measures and accommodative financial conditions, business fixed investment is likely to remain on an increasing trend, including labor-saving and digital-related investment to address labor shortages, as well as research and development (R&D) investment.

Household sector: regarding the employment situation, labor market conditions are likely to tighten further as the economy improves, with it becoming more difficult for labor supply of women and elders to increase. Against this backdrop, it is likely that a wide range of firms will continue to raise wages steadily in this year’s annual spring labor-management wage negotiations, following the solid wage increases last year, and the growth in nominal wages is projected to remain relatively high. Although private consumption is expected to be more or less flat for the time being due to the remaining impact of price rises, it is projected to gradually return to a moderate increasing trend, with a continued rise in employee income. Meanwhile, private consumption is projected to be underpinned by the government initiatives such as the measures to reduce the household burden of higher energy prices and the tax reform in fiscal 2026.

Housing investment is expected to continue recovering for the time being; thereafter, however, it is likely to follow a moderate declining trend, mainly reflecting a rise in housing prices and demographic developments. Public investment is expected to be more or less flat, and government consumption is expected to increase moderately reflecting factors such as an uptrend in healthcare and nursing care expenditures and a rise in defense-related spending.

Comparing the projections with those presented in the previous Outlook Report, the projected real GDP growth rate for fiscal 2025 is somewhat higher due to higher-than-expected growth in overseas economies and the impact of the statistical revision to the GDP figures. The projected growth rate for fiscal 2026 is also somewhat higher, mainly reflecting the effects of the government’s economic measures. The rate for fiscal 2027 is somewhat lower due to the dissipation of the effects of these economic measures.

Meanwhile, the potential growth rate is expected to rise moderately. This is mainly because productivity is likely to increase due to advances in digitalization and investment in human capital, and because capital stock growth is projected to accelerate due to a rise in business fixed investment. Potential growth is likely to be supported by the government’s various measures and other factors.

Baseline Scenario of the Outlook for Prices –

The outlook for the CPI (all items less fresh food) depends on the assumptions regarding crude oil prices and the government’s measures. Crude oil prices are assumed to be more or less flat throughout the projection period, based, for example, on developments in futures markets. Regarding the government’s measures, the abolition of the former provisional gasoline tax rate, measures to reduce the household burden of higher electricity and gas charges, and measures to make high school tuition and elementary school lunches effectively free, among other measures, will push down the year-on-year rate of increase in the CPI (all items less fresh food), particularly in fiscal 2025 and 2026.

Looking at the CPI (all items less fresh food and energy), which is not directly affected by fluctuations in energy prices, the year-on-year rate of increase is likely to decelerate to around 02%, mainly due to the waning of the effects of the rise in food prices, such as rice prices. Thereafter, with moves to pass on wage increases to selling prices continuing, the rate of increase in this CPI is likely to remain at around the same level.

The main factors that determine underlying inflation are assessed as follows. The output gap, which captures the utilization of labor and capital, has followed an improving trend, albeit with fluctuations. Based on the aforementioned outlook for economic activity, it is likely that the output gap will widen moderately within positive territory. Meanwhile, labor market conditions have tightened to a greater extent than can be explained by the changes in the output gap, partly due to a deceleration in the pace of increase in labor force participation of women and seniors. In this situation, upward pressure on wages and prices is likely to be stronger than suggested by the output gap, given that firms in many industries have started to face labor supply constraints.

Medium to long-term inflation expectations have risen moderately. Regarding the outlook, as the economy continues to improve and labor market conditions tighten further, firms’ active wage- and price-setting behavior is expected to become more widespread, and it is therefore likely that inflation expectations will continue to rise moderately and be at around 02% in the second half of the projection period.

Risks to Prices –

The first is firms’ wage- and price-setting behavior and its impact on inflation expectations. Firm’s behavior has shifted more toward raising wages and prices, and it is highly likely that the mechanism in which wages and prices rise moderately in interaction with each other will be maintained. On this basis, moves to reflect wages in selling prices could strengthen to a greater extent than expected, and there could be growing expectations that labor market conditions will tighten further; these developments could heighten upward pressure on wages. In this situation, there is also a possibility that both wages and prices will deviate upward from the baseline scenario, accompanied by a rise in medium to long-term inflation expectations. On the other hand, if the impact of tariffs on corporate profits, for example, becomes prolonged, this could lead firms to focus more on cost cutting. As a result, moves to reflect price rises in wages could also weaken.

Meanwhile, the recent rise in food prices, such as rice prices, largely reflects temporary supply-side factors, and it is therefore expected that the contribution of this rise to the CPI will gradually wane. That said, if new temporary factors, such as irregular weather events, arise or if the pass-through of increased personnel expenses and distribution costs to selling prices strengthens, the rise in food prices could persist for longer than expected.

Since consumers purchase food items on a frequent basis, if the price rises persist, the CPI could be pushed up through changes in inflation expectations. On the other hand, it is also possible that the CPI could be pushed down, as private consumption could decline through a deterioration in household sentiment.

The second risk is future developments in foreign exchange rates and import prices, including international commodity prices, as well as the extent to which such developments will spread to domestic prices. This risk may lead prices to deviate either upward or downward from the baseline scenario.

Uncertainties remain over the outlook for the global economy, such as the impact of trade policies, which could lead to a rise in import prices from the supply side or to significant fluctuations in foreign exchange rates and international commodity prices. In this regard, attention should be paid to the point that, with firms’ behavior shifting more toward raising wages and prices recently, exchange rate developments are, compared to the past, more likely to affect prices, and that such moves could affect underlying CPI inflation through changes in inflation expectations.

Team Maverick.

Museums will be named after India’s National Heroes, not invaders: Chief Minister

Grand museum named after Chhatrapati Shivaji Maharaj being constructed at a rapid pace: CM…

Museums will be named after India’s National Heroes, not invaders: Chief Minister

Grand museum named after Chhatrapati Shivaji Maharaj being constructed at a rapid pace: CM …