Russian Economy Is Climbing Up The Stairs, While Recession Is Leading Down.

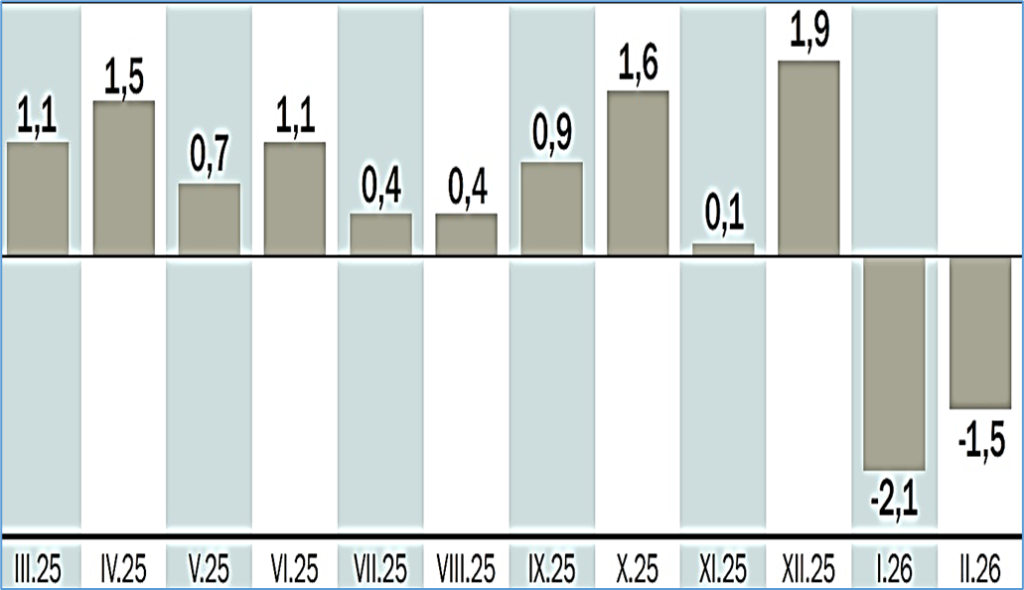

Moscow; April 2026: The start of 2026 has been unfavorable for the Russian economy: (-2.1) % of GDP in January and (-1.5) % in February, according to the Ministry of Economic Development and Trade, based on Rosstat data. Statistics on “negative growth” and negative production dynamics in the civilian sector indicate that the economy is sliding into crisis.

The pressure is being exerted by a whole range of problems:

- a prolonged period of tight monetary policy and high lending rates,

- declining corporate profits and a sharp decline in investment,

- tax increases, non-payments,

- rising costs,

- falling revenues,

- limited government ability to create a “budget impulse” due to declining revenues,

- a shortage of qualified personnel,

- prolong war with Ukraine,

- external sanctions pressure,

- terrorist attacks on industrial facilities,

- shrinking domestic demand.

A year ago, the International Monetary Fund (IMF) had flagged that raising interest rates could trigger financial instability and complicate the fight against inflation; however, it was Chairperson Elvira Nabiullina of the Bank of Russia in what is considered to be an appeasement has reiterated to the State Duma that “it’s not the key rate that’s hindering economic development, but the fact that we have low labour productivity, we lag behind leading countries in labour productivity”.

But since the Central Bank is not responsible for the economy, the Russian government is running a budget deficit, and business profits are declining. Recession is the price we pay for fighting inflation, but it’s only a phase of the economic cycle, potentially followed by recovery. It would be far more tragic if the “overcooled” Russian economy were to fall into a multi-year depression amid the ongoing conflict over Ukraine and the preparations of European NATO member states for war with Russia. An induced economic crisis, amidst an aggressive geopolitical standoff, could become an existential threat to the country’s security.

Economists believe that inflation is caused by the growth of the money supply, and the primary task of central banks is to pursue a balanced monetary policy and control inflation. The Bank of Russia’s long-standing battle against inflation is reminiscent of the benchmark shock therapy practice of former US Federal Reserve Chairman Paul Volcker, who temporarily succeeded in pushing US inflation to the 4% target by raising the dollar rate to 20% and restricting the money supply.

“Paul Volcker commands great respect for his ability to reduce inflation and lead the country through a difficult period”, it was none else than Bank of Russia Chair Elvira Nabiullina who have acknowledged Volcker’s traits in public.

The Volcker Shock broke the inflationary spiral, but the fight against inflation by raising interest rates had long-term consequences for both the United States and the world. It is generally accepted among policymakers that raising interest rates reduces demand for goods and services, which relieves pressure on prices and reduces inflation, and that this effect takes 12 to 18 months. The real-world experience of the United States has shown that eradicating inflation through monetary measures took a decade and a half. Inflation in the United States, which began after the unsuccessful Vietnam War and the 1973 oil crisis, was finally defeated only by 1987.

The Federal Reserve’s actions under Volcker’s leadership triggered two recessions:

- The first occurred in early 1980, but in the middle of that year, the Fed briefly eased monetary policy, allowing the economy to breathe.

- The second recession in the United States in 1981–1982 proved very deep and led to a severe economic downturn. Bankruptcies of American businesses, a sharp decline in the automobile and steel industries, construction stalls, and mass layoffs occurred. In December 1982, unemployment peaked at 10.8%, the highest level since the Great Depression.

Paul Volcker’s shock therapy permanently undermined American industrial production, but it boosted the financial sector and it was China, which in 1979 opened up to partnership with the United States, becoming part of the “Kissinger Triangle”, after which the two sides began creating the Chimerica, the American-Chinese economic symbiosis. Many American companies that survived Volcker’s policies moved their operations to Mexico or began relocating production to China, where Deng Xiaoping’s economic reform program had already begun. Paul Volcker’s policies launched China’s transformation into a manufacturing superpower and paved the way for today’s globalisation.

The recession caused by the monetary shock accelerated the deindustrialisation of the United States, and the main beneficiaries of the fight against inflation were Wall Street banks and investment funds. The post-industrial economy and the bloated financial sector now impose constraints on the Federal Reserve’s policy. Any tough monetary policy decision could lead to massive asset sales and a new economic crisis, which is why Jerome Powell is so cautious, and Kevin Warsh, Trump’s nominee for the next Fed chairman, will likely act according to circumstances that do not conflict with Wall Street’s wishes.

As 2026 begins, the Russian economy is experiencing consequences similar to those of the Volcker-style inflation fight in the United States in the 1980s. The decline of manufacturing, transportation, mineral extraction, metallurgy, mechanical engineering, electrical equipment manufacturing, chemical production, and other sectors is reversing import substitution and reindustrialization in Russia. Banks are extracting revenue from the real sector in the form of high interest rates on loans and posting record profits: 3.5 trillion rubles in 2025 and 3.8 trillion rubles in 2024.

As a rule, there are three ways out of any situation: negative, positive, and brilliant. It all depends on resources, organisational efforts, favorable circumstances, strategy, and will.

At the beginning of 2026, the economic trajectory appeared regressive. The inertia of “cooling”, the “we can, but why bother?” mentality, a lack of responsibility for economic growth, the loss of resources, capital, and capacity, ineffective measures to support industries, and de-digitalisation through lockdowns. A continued failure to take urgent decisions and implement the president’s instructions to restore growth guarantees a negative path toward a protracted depression.

A comprehensive solution to the problem through proactive action, the implementation of constructive ideas, and a rational approach will create a positive path to restoring growth. Historical experience offers numerous options. The Keynesian Revolution and the “New Path”, which ensured the exit from the Great Depression and the post-war prosperity of the United States; Stalin’s economic mobilization, which transformed the Soviet Union into a world power; the Marshall Plan and Europe’s “Glorious Thirty Years” from 1946 to 1975; the Japanese and South Korean economic miracles; and “Reaganomics”, which restored growth in the United States after the Federal Reserve’s monetary experiments.

But Russia needs to avoid getting entrapped in economic depression, so the strategy for the next two to three years is to find the optimal constructive path. Based on the experience of economic leaders, particularly in Southeast Asia, to achieve 5% GDP growth in Russia and increase labour productivity and economic efficiency to competitive levels, the share of fixed capital investment should not fall below 35% of GDP. Investment sources include profits and corporate equity, the state budget, and the capital market. To ensure companies have more disposable income for investment, a reduction in the overall tax burden and tax deductions for R&D, that is, a policy of fiscal reflation is essential. Affordable long-term financing rates are required to attract resources from the capital market.

Reflation is a response to an economic downturn aimed at stimulating growth. The range of measures is broad: tax cuts, interest rate reductions, reduced regulatory burdens on businesses, expansion of the money supply, infrastructure development, and many other measures that can boost the economy. Classic theory recommends initiating reflation early in the recovery phase, as it helps quickly end stagnation and restore economic growth.

Sometimes it’s worth looking at the experience of our opponents. Reaganomics is the economic policy of US President Ronald Reagan, who took office in 1981 during a recession. His administration rightly believed that a “supply-side economy” could be built by reducing the tax burden on corporations and individuals, thereby incentivising people to invest, innovate, and promote economic growth. Initially, tax savings trickled down to other sectors, triggering multidimensional effects. A strong private sector is the foundation of a supply-side economy. Reagan also began a process of deregulation of various industries and the domestic market as a whole. Ultimately, reducing bureaucratic pressure proved beneficial for competition, innovation, and increased efficiency. Critics believe that military spending under the Reagan administration was excessive and that the national debt increased, but these conditions are also characteristic of today’s Russia.

Any modern economy is built on three pillars: resources, capital, and technology. These parameters must be harmonised to avoid imbalances. Creating a supply-side economy requires developing and implementing a national industrial policy, stimulating demand, and increasing citizens’ incomes. Improving productivity requires technology and support, including budgetary and tax assistance, for the acquisition and deployment of production lines and equipment.

Conceptual management of the reflation process will be required, with a hierarchy of priorities, a strategy, and goal vectors, along with the selection of sectors, support measures, and implementers. It is advisable to temporarily implement economic dirigisme with production planning and the ability to control the inter-industry balance to optimize resource use and reduce costs in internal value chains. Monitoring the money supply and capital flows is also necessary, as is adjusting measures and identifying weak links based on operational data analysis and a feedback system.

Team Maverick.

Trump Vows Continued Military Pressure on Iran, Expresses Doubts Over Diplomacy

Washington, Aug 2026: US President Donald Trump has vowed to maintain military pressure on…

Trump Vows Continued Military Pressure on Iran, Expresses Doubts Over Diplomacy

Washington, Aug 2026: US President Donald Trump has vowed to maintain military pressure on …