Open Market Trading Desk At The Federal Reserve Bank Of New York Has Published Its Annual Report.

New York; April 2026: The Open Market Trading Desk (Desk) at the Federal Reserve Bank of New York has published its annual report today early morning (IST; late evening local time), Open Market Operations During 2025.

This report was prepared by the Markets Group and presented to the Federal Open Market Committee (FOMC). It contains a summary of open market operations conducted by the Desk for the System Open Market Account (SOMA) and a review of Federal Reserve balance sheet developments in 2025. The report also presents New York Fed staff projections of SOMA domestic securities holdings, reserve balances, and associated net income. The projections are based on assumptions drawn from FOMC communications and the January 2026 Survey of Market Expectations.

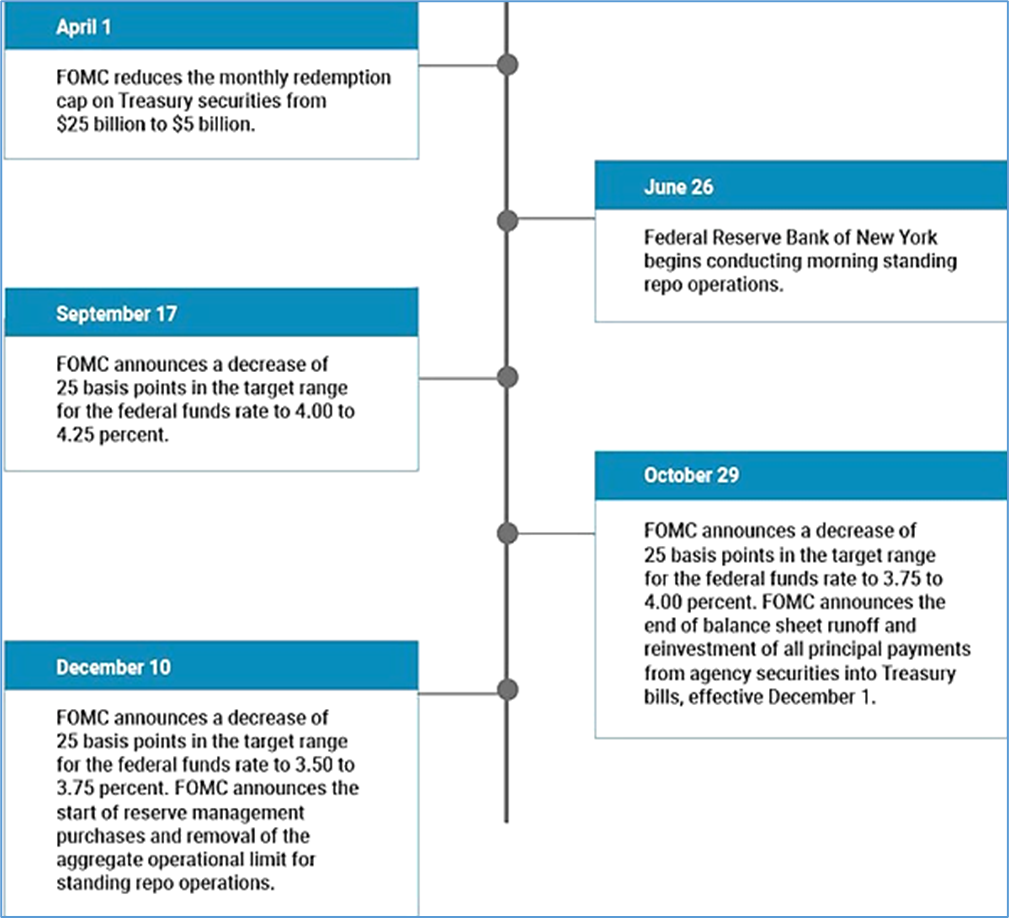

During 2025, the economy grew at a moderate pace, while the labour market cooled further and inflation remained somewhat elevated. The Federal Open Market Committee (FOMC or Committee) decreased the target range for the federal funds rate by a quarter percentage point at each of its final three meetings of the year, ending the year in a range of 3½% to 3¾%.

The Federal Reserve’s monetary policy implementation framework continued to operate as expected and the effective federal funds rate (EFFR) remained in the target range throughout the year. The System Open Market Account (SOMA) portfolio continued to run off through the end of November. The cumulative effects of runoff coupled with significant U.S. Treasury issuance resulted in spreads of U.S. Treasury repo rates to interest paid on reserve balances (IORB) increasing sharply into the latter part of 2025. Spikes in these spreads were more pronounced around financial reporting and Treasury settlement dates.

As a result of persistently higher secured money market rates, the EFFR began to increase relative to the IORB rate beginning in late September and ended the year at a spread of 1 basis point under the IORB rate, compared to 7 basis points under the IORB rate at the beginning of the year. Consistent with these shifts in the EFFR-IORB spread, a broad set of indicators suggested that total reserves had

moved close to levels the FOMC considered to be ample. As a result, the FOMC decided at its October meeting to end balance sheet runoff effective December 1, in line with its Plans for Reducing the Size of the Federal Reserve’s Balance Sheet.1 Then, at its December meeting, the Committee decided that reserves had reached ample levels and directed the Open Market Trading Desk at the Federal Reserve Bank of New York to increase SOMA holdings of Treasury bills and, if needed, coupons up to three years to maintain ample levels of reserves going forward. An ample supply of reserves enables the Federal Reserve to influence the level of the federal funds rate and other short-term interest rates primarily through its administered rates, rather than by actively managing the supply of reserves.

During the year, total assets of the Federal Reserve decreased by $184.8 billion, largely due to the runoff of SOMA securities. The FOMC slowed the cap on monthly runoff of Treasury securities in April, while leaving the cap on agency securities unchanged through November, resulting in agency securities making up most of the SOMA runoff during the year. Federal Reserve assets as a percentage of nominal GDP declined to 22% by yearend, compared to 24% at year-end 2024. The balance sheet reduction process that began in mid-2022 reduced SOMA securities holdings by a cumulative amount of over $2 trillion.

Federal Reserve liabilities declined during the year in line with assets, while their composition changed due to significant shifts in usage of overnight reverse repurchase agreement (ON RRP) operations and the Treasury General Account (TGA). ON RRP usage dropped to near-zero levels by the second half of the year, as investments outside the ON RRP became more attractive. The TGA saw significant variations due to dynamics around the debt ceiling episode, with usage significantly decreasing in the first half of the year, followed by a sharp rebuild thereafter. These trends, along with the cumulative impact of the SOMA runoff, resulted in the level of reserves beginning to drop in August. Average Reserve Levels in December 2025 were $322.3 billion lower compared to 2024, reaching $2.85 trillion at the end of 2025.

As reserves declined nearer to ample levels heading into the latter half of the year and U.S. Treasury issuance remained robust, broader secured funding rates trended higher and were more volatile, particularly around period end and Treasury settlement dates. This volatility resulted in wider SOFR-IORB spreads and drove more material usage of standing repurchase agreement (SRP) operations.

Higher SRP usage in the second half of 2025 highlighted the SRP’s role in dampening upward pressure on overnight money market rates, supporting smooth market functioning, and promoting effective policy implementation in an ample reserves environment. To strengthen the effectiveness of SRP operations, two modifications were implemented in 2025. In June, following several technical exercises, the Desk added an additional morning SRP operation on an ongoing basis, allowing participants to receive funds earlier in the day, when repo trading is most active. In December, the Federal Reserve removed the aggregate operational cap on standing overnight repo operations, effectively moving the SRP to a full-allotment format.

Global U.S. dollar funding markets remained stable during 2025 amid ample dollar liquidity, and usage of U.S. dollar central bank liquidity swap lines was modest. In addition, usage of the standing overnight repurchase agreement facility for foreign and international monetary authorities (commonly referred to as the FIMA repo facility) was limited throughout the year. The Desk did not conduct any foreign exchange intervention activity for the SOMA during 2025 and continued to manage the SOMA foreign currency reserve holdings in line with the portfolio’s investment objectives of liquidity, safety, and return.

During 2025, SOMA net income plummeted to (-$10.8 billion), compared to (-$74.7 billion) in 2024. This change was driven by reduced interest expense due to lower administered rates and decreases in interest-bearing liabilities. The Federal Reserve’s deferred asset ended the year at $243.5 billion, compared to $216.0 billion in 2024, reflecting the cumulative negative net income of the Federal Reserve. The deferred asset is expected to decrease in the future as net income becomes positive.

The deferred asset has no implications for how the Federal Reserve implements monetary policy and does not constrain its ability to meet its financial obligations. The market value of the SOMA securities portfolio fluctuates with changes in the level of interest rates and ended the year with an unrealized loss position of $844.2 billion, compared to $1.06 trillion at end-2024.

Unrealized gains or losses have no effect on net income or remittances to the Treasury or on the ability of the Federal Reserve to conduct monetary policy. In coming years, the size and composition of the balance sheet will continue to evolve. A projections exercise shows the evolution of the balance sheet under a set of simplifying assumptions around the growth of Federal Reserve liabilities, based on the Desk’s January 2026 Survey of Market Expectations. Under these projections, the portfolio expands through reserve management purchases to accommodate the growth in Federal Reserve liabilities.

Portfolio holdings shift toward Treasury securities over time, consistent with the FOMC’s stated intention to return to a portfolio composed primarily of Treasury securities. Using survey-based assumptions about the path of interest rates, total SOMA net income remains positive over the projection horizon.

Operational resilience remains an important priority, and during 2025, the New York Fed continued to maintain its operational flexibility, along with its geographic resilience. The Desk continued its practice of undertaking small-value exercises with counterparties to maintain readiness for a range of potential FOMC directives.

Timeline Of Selected Events:

Team Maverick.

Tripura: Government Implements People Centric Governance ‘Mukhyamantri Samipeshu’.

Agartala; June 2026: The Tripura government’s flagship public outreach initiative, &…

Tripura: Government Implements People Centric Governance ‘Mukhyamantri Samipeshu’.

Agartala; June 2026: The Tripura government’s flagship public outreach initiative, “Mukhyamantri Samipeshu”, has emerged …